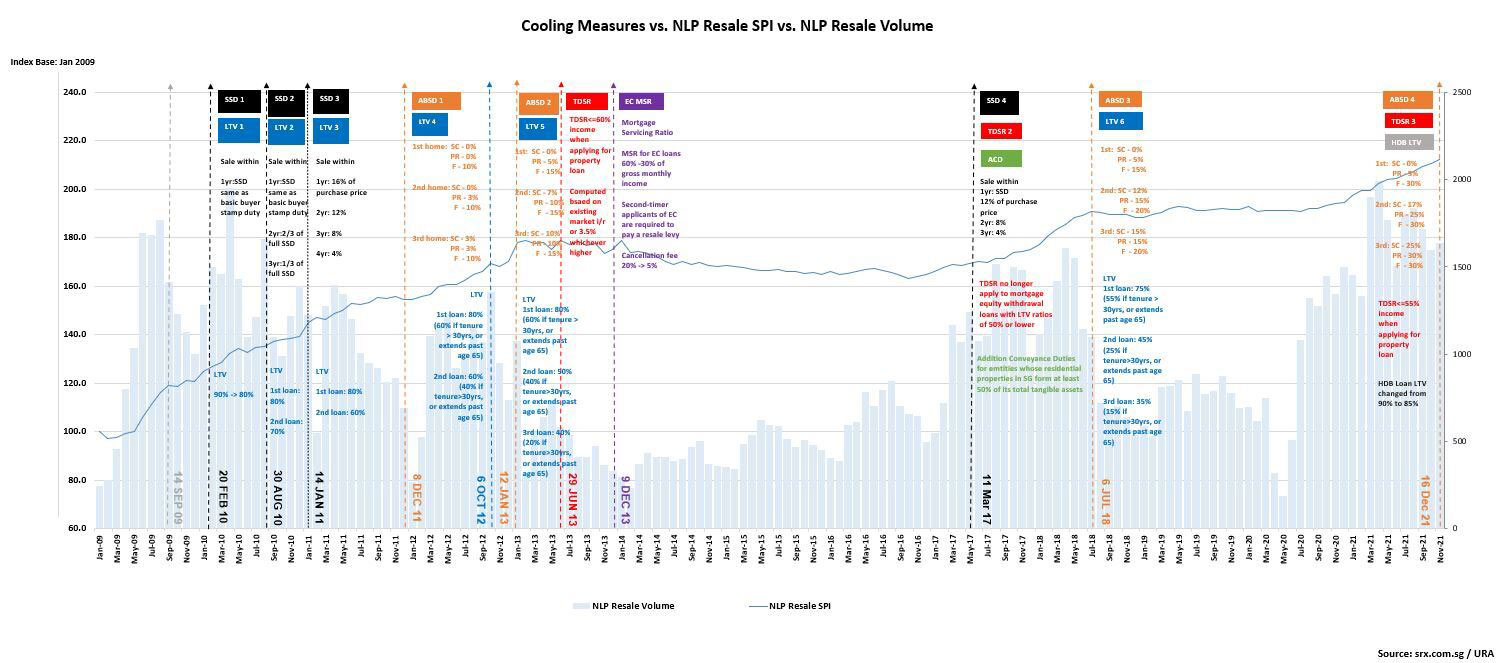

Singapore is a tiny country that has gone against all odds to be where it is today and continues to face challenges from global influences due to our interlinked economies. Ever since the United States subprime mortgage crisis, the Additional Buyer’s Stamp Duty (ABSD) was introduced in 2011 to moderate demand for residential property, thereby ensuring that residential property prices move in tandem with economic fundamentals.

Good old days where we could take 90% loan to value and own multiple residential properties are now not as easy to achieve. Those who were wounded by the economic crisis might be fearful of getting into the property market again. First let us look at what has changed with ABSD.

Purpose of ABSD

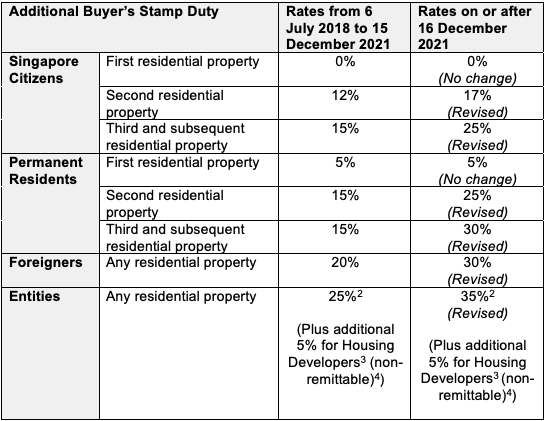

Basically the regulations strengthens the foundation of residential property and keeps it affordable for Singaporeans, preventing the risk a drastic price correction in the future which could have a devastating effect. ABSD for Singapore Citizen (SC) buying their 2nd property in particular started from 7% to 12% to the current 17% that was recently revised in Dec 2021. The largest impact were towards foreigners on their 1st property who were slapped with 10% to 15% to 20% and now 30% ABSD.

Effects of ABSD

This protection cuts both ways, which means that while residential property in Singapore will unlikely see drastic prices decrease it will also be unlikely for prices to increase sharply. The following chart compares the property price index for various big cities and you can see that Singapore has a much smaller price increase in comparison.

With the various stamp duties in place, Singapore has come out stronger than many big cities after COVID attracting wealthy individuals who favor safe havens for wealth preservation, alongside London which has been a long time favorite. This table shows how strong the demand for housing is in Singapore with high population and GDP growth, while having one of the lowest unemployment rate. 2023 forecasts even stronger numbers

How to avoid the ABSD and own your 2nd property?

After explaining the purpose of ABSD and explaining the risks of residential property in Singapore, let us go into how we can avoid the ABSD with the objective of owning a 2nd property.

Let us start with a typical profile of a Singapore Citizen (SC) married couple who are purchasing a HDB as their first home.

- Buying as a single owner instead of as a couple for HDB

- Decoupling for private residential property

- Purchasing under child name (above 21yrs)

- Purchasing under trust (usually when child is under 21yrs)

- Purchasing other type of property that do not incur ABSD

- Inherit properties under will or intestate law

If you or your spouse is a Permanent Resident (PR) or foreigner, you would have to pay ABSD even for your first home. What are some of the ways you can reduce or avoid paying the ABSD?

- Purchase with a Singaporean spouse

- Apply to become a PR or SC

- Using the privilege under the Free Trade Agreements (FTAs)

#1 - Buying as a single owner for hDB

Filled with excitement for your first home, most young couples would be thinking about how they want to renovate their first home instead of thinking how they would like to hold the property. Since HDB requires buyers to form a family nucleus, most assume that the HDB has to be owned by both husband and wife under the legal holding called joint tenancy.

Application has to be as a family but many do not know that it can be owned by just one party with the spouse as an essential occupier. After the 5 years minimum occupancy period (MOP), the occupier can purchase a private property and will not be subjected to ABSD as it is considered the first property ownership.

Requirements

- Only the owner’s CPF ordinary account funds can be used

- Income requirement for home loan is based purely on the owner

#2 - Decoupling for private Residential property

This option is for those who currently co-own a private residential property or an Executive Condominium (EC) that has reached it’s 5 years MOP. Owner A may transfer the share of ownership to owner B, usually by way of sale. Owner A would be free of property count and be able to purchase a residential property and not be subject to ABSD.

As buyer stamp duty is payable based on the market value of the share being transferred, co-owners who plan to do this should hold their first property in a 99% and 1% tenancy in common structure. The party exiting should hold the 1% ownership.

Both owners are required to be represented by 2 different law firms to process the conveyancing. If there is outstanding mortgage loan, there could be some mortgage loan restructuring fees and penalties. Restructuring mortgage can take up to a month or more while the legal conveyancing can take place in a matter of days.

Requirements

- Buyer has to take over the existing mortgage loan solely

- Return the CPF used by the outgoing party

#3 - Buying under a child's name (>21yrs)

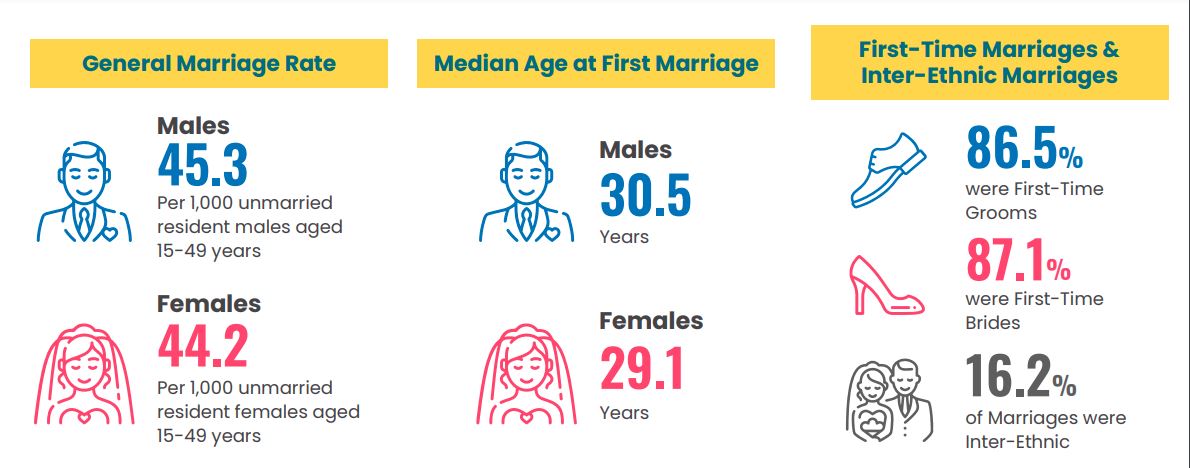

You might have accumulated a small fortune and started thinking about your retirement. Commonly this is when parents hit 50 and your child might have just graduated or started work. Recently starting pay is averaging higher but usually there is not enough cash or CPF accumulated for a down payment until about 30 years old for a private home.

The usual concern is in applying for a Build To Order (BTO) flat or new EC, they would have to dispose any private property 30 months prior to application. If you child is not attached, marriage and home purchase plans are likely not in the near horizon. Looking at the median age of marriage we can estimate the time frame available.

Alternatively this home can be given to your child or if their future spouse has his/her own property that they can move into, their home ownership would not be a problem. While this plan is the easiest to execute, there is a shorter investment timeframe with uncertain changes dependent on your child.

The advantage of this method is the long loan tenure of up to 35yrs because of your child’s age, lowering monthly installment to enjoy positive cash flow. However having a property under another person’s name even if it is your own child can sometimes be complicated.

Requirements

- Not planning to apply for BTO or new EC anytime soon

- Trust that your child would not run away with a property under them

- Your child needs to qualify for the mortgage loan

- Down payment likely in full cash.

#4 - Buying a property under trust (child under 21yrs old)

Before you get too excited, this is a full cash option and a 35% ABSD has been implemented in May 2022 to close this loophole. You can get a full refund of the 35% when conditions are met but I shall not explain too much about this method since it is beyond reach for most.

If you are considering this method, you would be speaking to your lawyer or you may speak to me privately.

#5 - Properties not subjected to ABSD

Commercial, industrial, overseas property and REITs are common types that are not subjected to ABSD. Take note that residential transactions are on average more than 40 times of commercial and industrial. If you are not a business owner that have dealt with such properties, the learning curve and risks can be huge.

Recommend you understand corporate structure and how GST works as well as many sellers are corporate owners and GST registered. Have a specialized agent with experience in this area to assist you.

Overseas property have a totally different regulation depending on the country you are looking at. Common countries are in those who have children or business in that country to “keep an eye on”, such as Malaysia, Indonesia, Australia and London. Thailand, Vietnam and Cambodia have popular as well due to their affordability.

I usually recommend a backup plan or a 2nd use for property investment. Usually overseas properties have their use limited strictly to rental which gives you less flexibility.

Real Estate Investment trust (REITs) is a capital market product bought through your bank or stock brokerage. They are very liquid and require very little capital having a wide range of property types all over the world that are professionally managed, including data center, industrial storage, hospitality, commercial malls, healthcare, etc.

#6 - Inherit properties under will or intestate law

Transfer of property upon death is not subjected to any tax or duties. Depending on the type property being inherited and the what the heir owns, the heir can keep the inherited property even if the heir owns multiple properties. The 3 scenarios are;

- Heir owns a HDB that has completed the minimum occupancy period and is inheriting private property.

- Heir owns private property and is inheriting a private property.

- Heir owns private property and a HDB that was bought before 30th Aug 2010 is being inherited. If the heir is eligible to own a HDB flat and wants to keep both the private property and HDB, the heir must move into the HDB flat.

In conlusion

While I have shared various ways to avoid ABSD, it can still make sense to pay the 17% ABSD with an estimate of 5 years of renting to cover the ABSD cost and 7 years of renting to cover 25% ABSD. Make full use of your citizenship to own a private property for every individual as early as you can. Recycle the capital and upgrade to a bigger property if you would like to increase your investment.

There is no best route. Which direction you should take depends on your individuals situation.

Contact me for a 30 mins consultation to assess which solution suits you.